The much-anticipated nationwide private school choice program, established through the federal scholarship tax credit enacted nearly a year ago, will see its detailed regulations released by the U.S. Department of the Treasury no later than the end of September. This timeline, revealed in initial guidance issued by the Treasury Department, offers a glimpse into a program designed to provide taxpayers with a federal income tax credit for charitable donations to scholarship-granting organizations, which in turn will fund K-12 educational services, including private school tuition and public school expenses.

While the full proposed rule is undergoing legal review, a preview was presented by Kevin Salinger, deputy assistant secretary for tax policy at the Treasury Department, during a recent roundtable discussion. This gathering brought together key stakeholders, including scholarship-granting organizations, education representatives, technology providers, and state officials, to discuss the program’s implementation. Salinger indicated that once the proposed regulation is officially released, it will be applicable for tax year 2027, aligning with the program’s official commencement date of January 1, 2027.

This federal scholarship tax credit represents a significant development in educational policy, marking the country’s first nationwide private school choice initiative. The program, born from the "One Big, Beautiful Bill" legislation, aims to empower families with greater flexibility in choosing educational environments for their children. Taxpayers will be able to donate up to $1,700 annually to eligible 501(c)(3) scholarship-granting organizations, receiving a 100% federal income tax credit for these contributions. However, the crucial caveat is that scholarship awards will only be available to students residing in states that formally opt into the program.

To facilitate early planning, the Internal Revenue Service (IRS) has offered states an early opt-in process. As of April 15, a significant number of states, totaling 27, have expressed their intention to participate, signaling widespread interest in the program’s potential to expand educational options. This early commitment allows states and scholarship-granting organizations to begin formulating their strategies and operational frameworks ahead of the official regulatory release.

A Detailed Look at the Proposed Rule’s Preview

The preview of the proposed rule, summarized in a two-page document, addressed several key areas critical to the program’s successful implementation. While specific details were not fully elaborated upon in the initial preview, the Treasury Department’s commitment to clarity and accessibility was emphasized. Treasury Secretary Scott Bessent articulated this commitment in a recent statement: "At Treasury, we take seriously the work of implementing this federal tax credit faithfully and effectively. We are committed to providing certainty to states, scholarship-granting organizations, taxpayers, and families alike, as well as making certain that this process is easy to navigate."

The preview aimed to provide stakeholders with an initial understanding of the program’s architecture, paving the way for more concrete planning. The delay in the full release, attributed to ongoing legal reviews, underscores the complexity of establishing such a novel, nationwide program. The Treasury’s proactive approach in offering a preview and an early opt-in process demonstrates an effort to mitigate potential disruptions and foster a smooth transition into the program’s operational phase.

Program Mechanics and Taxpayer Benefits

The core mechanism of the federal scholarship tax credit involves a direct incentive for charitable giving towards education. By offering a dollar-for-dollar tax credit, the program aims to significantly reduce the financial burden on taxpayers who wish to support educational initiatives outside of traditional public school systems. The annual contribution limit of $1,700 per taxpayer is designed to encourage broad participation without creating undue financial pressure.

For scholarship-granting organizations, this program represents a potential surge in funding. These non-profit entities play a pivotal role in administering the scholarships, acting as intermediaries between donors and students. Their ability to effectively vet students, select appropriate educational institutions, and ensure the proper allocation of funds will be paramount to the program’s success. The preview likely touched upon guidelines for these organizations, including eligibility criteria for both donors and recipients, as well as reporting requirements to the IRS.

The opt-in mechanism for states is a critical component, reflecting a balance between federal initiative and state autonomy. Each state will have the discretion to decide whether to participate, allowing them to align the program with their existing educational policies and priorities. This approach acknowledges the diverse educational landscapes across the nation and provides states with the flexibility to tailor the program to their specific needs and circumstances. The fact that over half the states have already signaled their intent to participate suggests a strong consensus on the value of expanding educational choice.

Support and Opposition: A Divided Landscape

As the federal scholarship tax credit program moves through the formal rulemaking process, it has ignited fervent debate, drawing both strong support and significant opposition. Proponents herald the program as a transformative opportunity for millions of families, providing access to educational pathways that may better suit their children’s unique learning styles and needs.

Anne Lesser, president and CEO of the Invest in Education Coalition, a nonprofit advocating for school choice, expressed gratitude for the released guidance. In a statement, she highlighted the program as a "once-in-a-generation opportunity to access educational options and resources that best meet their children’s needs." This sentiment is echoed by organizations like ACE Scholarships, a national scholarship-granting organization. Norton Rainey, CEO of ACE Scholarships, conveyed his optimism, stating, "I am encouraged by the new guidance and hope final regulations provide a clear, consistent framework that removes unnecessary barriers for families and SGOs. The more streamlined and predictable the process is, the greater the program’s impact will be for students in every learning environment." These endorsements underscore the belief that increased educational choice can lead to improved student outcomes and greater family satisfaction.

Conversely, critics of the scholarship tax credit program, including many educators, policymakers, and advocacy groups, express deep concerns. They argue that the program, initially conceived under the Trump administration, represents an effort to divert much-needed resources away from public schools, which serve the vast majority of American students. Organizations like EdTrust have voiced apprehension regarding several facets of the program. Augustus Mays, vice president of partnerships and engagement at EdTrust, pointed to a perceived lack of accountability for student outcomes and insufficient state authority to ensure that taxpayer-generated scholarships are directed towards students with the greatest need. "The majority of our school leaders and educators in public systems want to make sure that what they’re doing is actually benefiting kids. This program is not set up that way," Mays stated, articulating a common concern among critics.

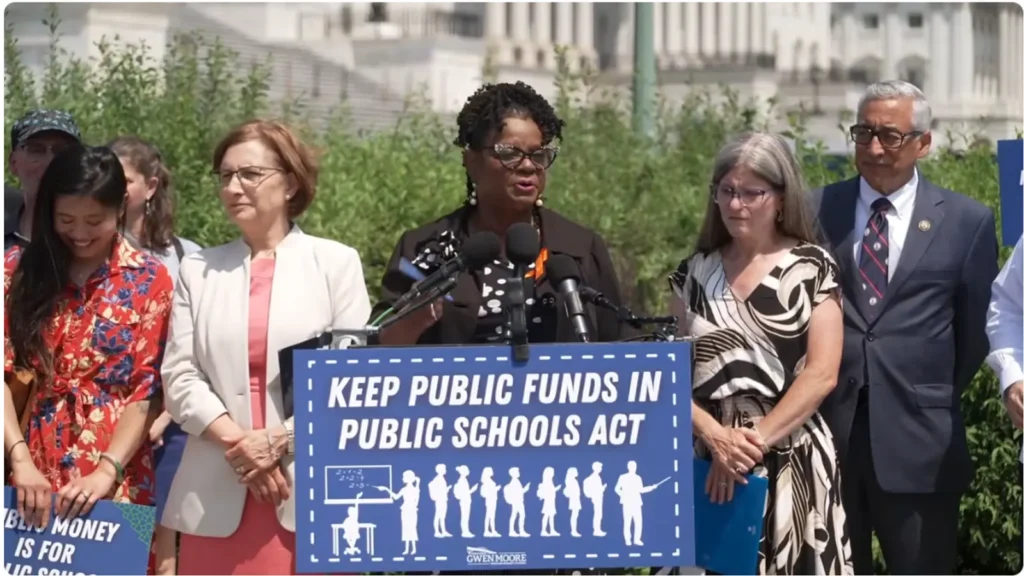

The opposition has also manifested in legislative action. Representative Gwen Moore, D-Wis., introduced the "Keep Public Funds in Public Schools Act" on Thursday, a bill explicitly aimed at repealing the scholarship tax credit provision. During a press conference in Washington, D.C., Moore characterized the program as a "voucher scheme" that would disproportionately benefit affluent students already enrolled in private institutions. She argued, "Your tax dollars should not go to fund private religious schools, who can pick and choose who they want to admit – no disabled students, no LGBTQ students, no Black students, no students who are not of a certain religion. We need to be investing in schools that serve the majority of America’s students and ones that accept every student regardless of their ZIP code." This perspective highlights concerns about equity, inclusivity, and the potential for the program to exacerbate existing educational disparities.

Broader Implications and Future Outlook

The implementation of the federal scholarship tax credit program carries significant implications for the broader educational landscape in the United States. On one hand, it promises to inject new resources into the private school sector and offer families more diverse educational choices, potentially fostering competition and innovation among schools. This could lead to improved educational quality as schools strive to attract and retain students in a more choice-driven market.

On the other hand, the program’s critics warn of potential adverse effects on public education. They argue that any shift of funds, even indirectly through tax credits, could undermine the financial stability of public schools, which often struggle with underfunding. This could lead to larger class sizes, reduced resources, and diminished educational opportunities for students remaining in the public system. The debate over resource allocation and the role of public versus private education is a long-standing one, and this new federal program is poised to intensify these discussions.

The success of the program will likely hinge on several factors: the clarity and fairness of the final regulations, the effectiveness of scholarship-granting organizations, the willingness of states to participate, and the ongoing public discourse surrounding educational equity and accountability. The Treasury Department’s commitment to providing certainty and ease of navigation will be crucial in ensuring that the program achieves its intended goals. As the end of September approaches, the full scope and impact of this landmark federal initiative will become clearer, shaping the future of educational choice and funding for years to come. The ongoing dialogue between proponents and opponents will undoubtedly continue to influence policy and public perception as the program rolls out.